Making the Most of Your Legacy

December 16, 2019

New York-New Jersey Trail Conference

Title

Making the Most of Your Legacy

Body

On Sept. 8, I had the privilege of meeting the founding members of the Trail Angel Society and presented my ideas on how to maximize their legacies at their Founding Members’ Brunch, held at Trail Conference Headquarters. I was grateful for their engaged participation, as it made for an interactive discussion.

Echoing Trail Conference Life Member and fellow Trail Angel Society Founding Member Bob Ross, The Charles Schwab Guide to Finances After Fifty suggests, “…think about planning your estate as planning your legacy. It’s your opportunity to make your mark on the world – to help and protect the people you care about most. It is your opportunity to give back to your community, or university, or cause.”

What techniques can you use to help maximize this opportunity? We spent about an hour post-brunch talking about the use of donor-advised funds, qualified charitable distributions, and other techniques.

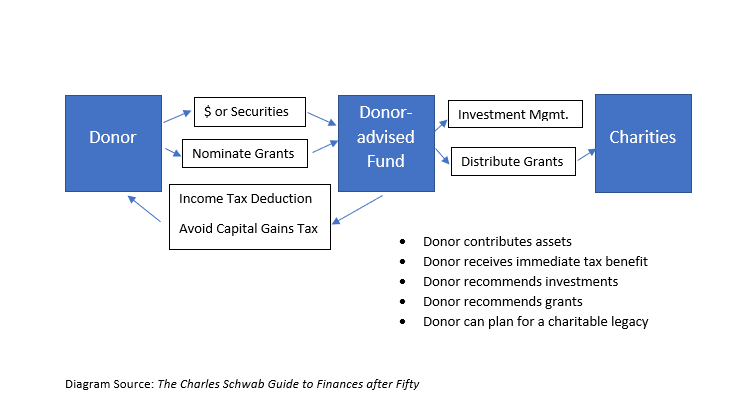

Donor-Advised Funds

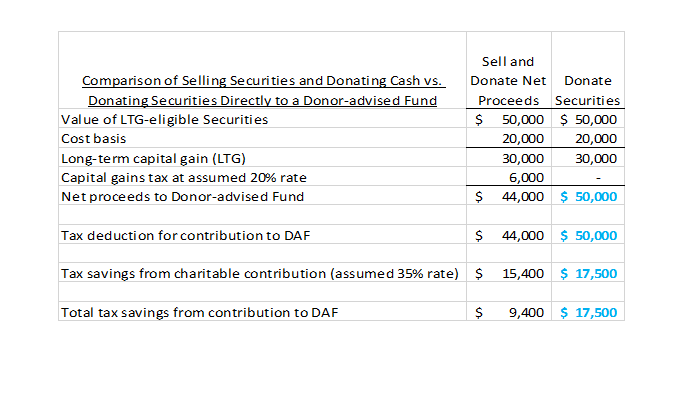

When you contribute to a donor-advised fund (DAF), you get an itemized tax deduction in the year contributed, and the DAF invests your contribution until you nominate grants to charities to be paid out by the DAF. There is no required time period during which you must nominate grants from the DAF to charity, and any investment income earned by the DAF on your contributed funds is not taxed to you. Even better, you may be able to avoid capital gains tax by contributing appreciated investments held for more than one year (e.g. long-term capital gain (LTG)-eligible securities), as the following example illustrates:

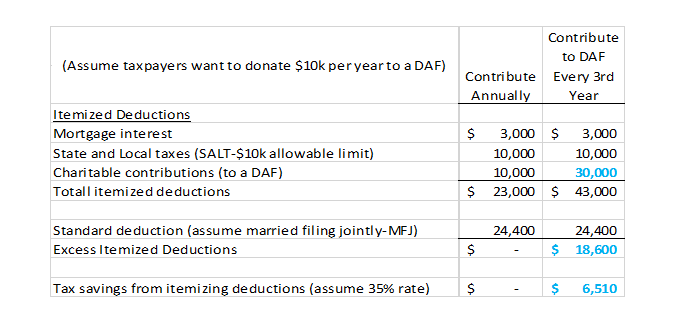

If you can’t itemize your deductions on your tax return each year, like many of us who reside in high-tax states (NY, NJ), consider whether “bunching” your charitable contributions into one year might enable you to itemize every second or third year instead:

After making their $30,000 “bunched” contribution to their DAF, the above couple could nominate a $10,000 annual grant to their favorite charitable organization, such as the Trail Conference, thereby helping Trail Conference to plan for a steady inflow of receipts.

Qualified Charitable Distributions

Another technique more uniquely available only to those who are at least 70 ½ years young is the qualified charitable distribution (QCD). When you reach this age, you’re required to begin taking taxable withdrawals from your traditional IRA accounts, otherwise known as required minimum distributions (RMDs). With a QCD, you can instead designate an amount, up to an annual limit of $100,000, to be paid directly from your IRA to a qualified charity (like the Trail Conference). This will satisfy all or part of your RMD in that tax year. Of course, a QCD makes sense only if you don’t need the money from an IRA withdrawal in a particular year. QCDs are a rare technique that enable you to save on taxes at both “ends” – you contributed to traditional IRAs on a pre-tax basis, and through a QCD, you can effectively take a non-taxable withdrawal from a traditional IRA (but only for a charitable purpose).

Other Techniques

Finally, a few other legacy-maximizing techniques that we discussed include beneficiary designations, charitable trusts and charitable gift annuities. You can name a charitable organization like the Trail Conference as beneficiary of your traditional IRA; you won’t receive an income tax deduction, but the organization will receive the proceeds tax-free after you die. Charitable trusts can be useful in more complicated planning situations where you may want a trust to provide income to certain beneficiaries for a period of time, and the remainder to other beneficiaries. You can designate a charitable organization(s) as an income or remainder beneficiary, depending on the type of trust that you establish. You’ll receive a tax deduction for the present value of the amount to be received by the charity(s). Similarly, charitable gift annuities allow you to contribute a lump-sum to a charitable organization, part of which is used to purchase an annuity that provides income to you or someone you designate for a period of time (e.g. 10 years). You’ll receive a tax deduction for the amount contributed to the charitable organization, minus the cost of the annuity.

If you’re interested in learning more about your options, please feel free to get in touch at 201-848-6802 or [email protected].